by Darko Pilav

March 19, 2020

by Darko Pilav

March 19, 2020

In this article

Recently, Central Bank Digital Currency (CBDC) has emerged as a hot topic in the financial world. Several Central Banks are running analyses and studies investigating the technical and economic feasibility of the introduction of digital money and the impact it might have on monetary policy, liquidity, etc.

In a series of posts, we will cover various aspects of this topic, including economic significance, modeling approaches and properties, and what benefits distributed ledgers might bring for CBDC. This first entry will answer questions like, What is CBDC exactly? How does it differ from physical cash and the money on your bank account? Why is it such a big deal, and why would it impact financial institutions?

What is CBDC ?

CBDC is a digital form of currency that is backed by a Central Bank and through that has legal tender status. This definition means it is recognized by law as a means to settle debts or meet financial obligations such as tax payments.

How does CBDC differ from physical cash?

CBDC is indeed reasonably similar to the bills in your wallet. But storing and transacting with physical currency is very inefficient and tedious. A digital representation of that value would be much more convenient and efficient.

How does CBDC differ from the money in your bank account?

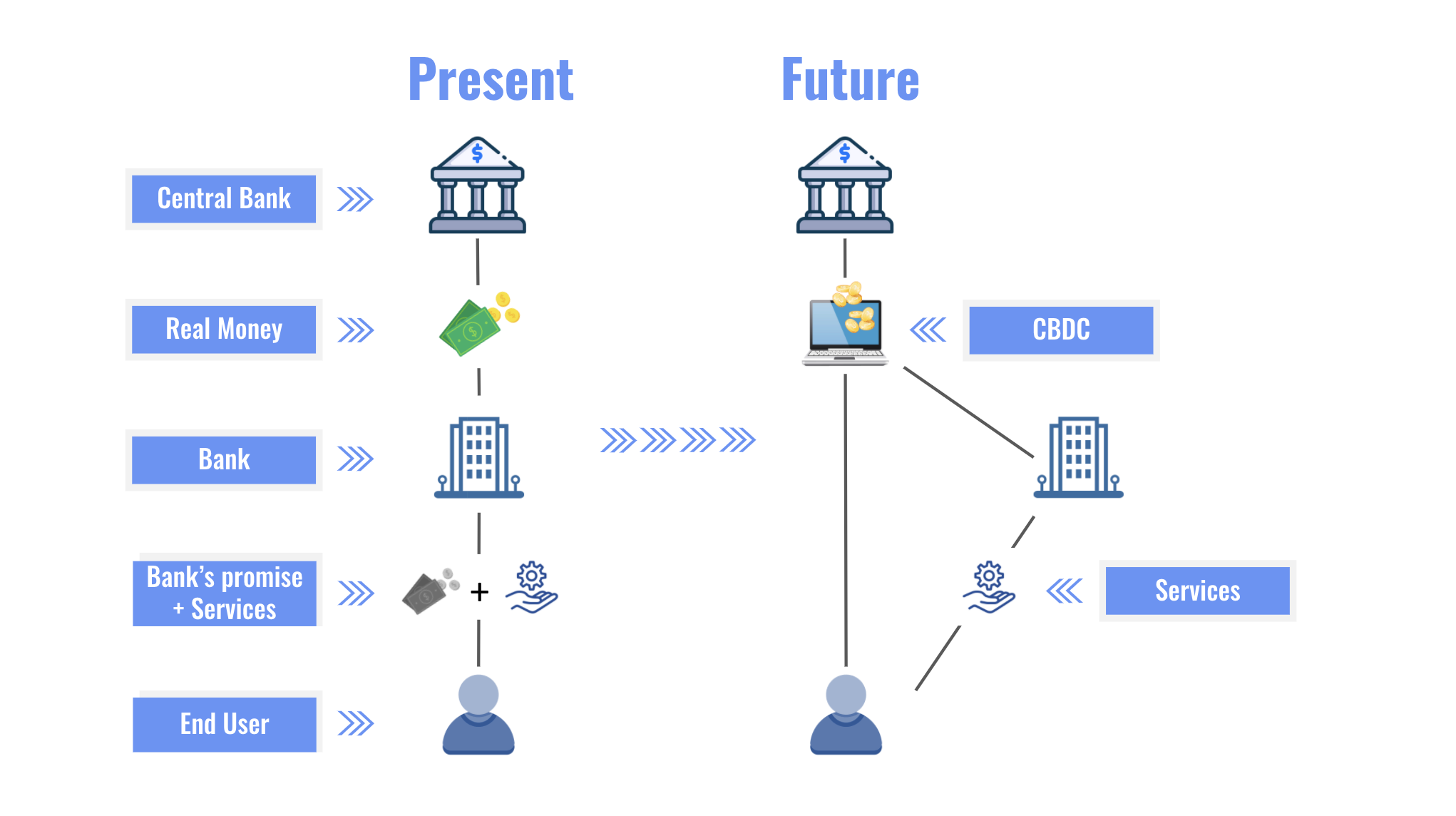

It is actually significantly different. The money you have with the bank is typically not legal tender. A dollar in your bank account is not the same as a dollar bill in your hand. It is much more a promise of the bank to give you a physical dollar upon your request. It is a bank's liability to fulfill those requests. Usually, a bank has no issues in fulfilling that promise, hence the line between your money in the account and the physical cash gets blurred. But if the bank ceases to function and goes bankrupt, this distinction makes all the difference. Because you don't hold a legal tender in your checking account but only the "bank's promise", so to say, it means that if the bank doesn't exist anymore, you can't hold anyone to your claim, and are effectively losing your money. What is even worse is that if enough people think that their bank might run into solvency issues, they will withdraw their money to save it from loss. If too many customers of a bank do that - called "a run on the bank" - the solvency of that bank is reduced additionally and can lead to the bank's collapse.

What are the benefits of CBDC?

CBDC has a couple of interesting favorable properties. The two most relevant ones are probably the following:

- Since CBDC would have legal tender status and would not be your bank's liability, you would not have to rely on the bank's solvency. Your money would be safe, no matter how well the bank does.

- The Central Bank would have a much more direct way to exert its monetary policy in that it would have a more potent tool to fulfill one of its main tasks: ensuring financial stability.

What would be the future role of banks?

Since owning CBDC would effectively mean that you have a relationship with - or an account at - the central bank, one could wonder what the banks would be doing?

Banks have a much better insight into the needs and wants of their customers than central banks. Hence, they can be much more innovative when it comes to services around the usage of money. A bank could distinguish itself through various financial services like a particularly useful mobile banking platform, new mobile payment methods, investment advice, or an excellent trading platform.

But one must also acknowledge that the banks' essential role of a loan giver would indeed be at risk. To understand why this is the case, we need to know how banks can give loans nowadays.

How do loans currently work?

As discussed earlier, when people deposit money at a bank, they get a promise from the bank to pay out cash upon request. Now let us assume that a business wants to take up a loan to be able to expand. After a vetting process, the bank gives them money under certain conditions, most importantly, the repayment schedule and the interest rate. This interest covers the administrative effort, the bank's profit, the interest payments for the depositors, and the risk of the loan-taking business going bankrupt and not being able to repay the loan.

So far, so good, but from where does the money for the loan come? It comes, among other sources, from the funds deposited earlier by the bank's customers. That is precisely the reason why if all the customers want to withdraw their funds, the bank wouldn't be able to pay everyone back. Hence, in the current system, the bank's capability to give out loans relies to an extent on the fact that it cannot cover all accounts at once.

What would be the effect of CBDC on the economy?

If a significant number of the bank's clients decide to hold CBDC instead of having a bank account like today, the bank would have less capital to give out loans, which would, in turn, make loans more expensive and potentially even not viable.

The implication is that a thoughtless implementation of CBDC without mitigating actions could have a drastic and adverse effect on the economy. It is probably one of the biggest reasons why central banks have not yet jumped at the opportunity to create a digital currency that would have legal tender status but are running analyses on how to solve the problem best.

What would be possible solutions?

There is not yet one final answer on how to mitigate the effect of CBDC on loans and banks' balance sheets. There are quite a few approaches to tackling this problem, and the real answer might lie in a combination of them.

For example, banks could transparently offer their customers that they deposit their CBDC so that they can use the capital for loans. The customers could choose to expose themselves to the risks we discussed above in exchange for interest, but they would do so well-informed and willingly.

Another approach would be for the banks to take out loans from the central banks to fund their customers' loans. Banks use such sources of capital already, and it would be primarily.

It is only a matter of time until the analyses provide the right combination of measures to implement.

Why should people prefer CBDC over bank accounts?

The main reason people would prefer CBDC over a bank account is that CBDC is not at risk when banks fail. The removal of that risk would be beneficial to individuals and the economy alike.

Furthermore, the transfer of money across banks and country boundaries becomes much more straightforward. Various bank systems would not need to interact with each other to facilitate such payments. All that is required is an update of the record at the central bank. This simplicity makes the process faster and cheaper.

There are further benefits.

- Money laundering could be easier to identify,

- There is a better chance for financial inclusion (i.e., people who can not afford a bank account, could have a CBDC account).

- There is potential for innovative payment systems and financial services.

- And many others...

Possible Future: The introduction of CBDC could remove risk from users, and allow banks to focus on services.

Final thoughts on CBDC

The introduction of CBDC might not be trivial. But there are ways to mitigate the problems, and the benefits for the broad population would be significant. We should strive for cheaper and quicker digital payments, more transparency about what your money is used for, and the possibility to make a conscious choice which risks you want to enter for which payout.

In the next instalment of this blog series, we will look at what technical properties a CBDC solution should have. We are going to explain how such a digital currency could look like using Daml.

Daml has also a new learn section where you can begin to code online: